Personal Loan vs. Credit Card: Which is Better for Short-Term Expense in SA?

Fast & flexible short term loans in South Africa from R100 to R5,000+

Apply NowDuring a financial disaster, such as a sudden car bill or a sudden home emergency, you need quick cash in your bank account. In South Africa, many people find themselves having to choose between using their credit card and applying for a short-term personal loan.

In South Africa all loans, whether from a bank or a payday lender, are governed by the National Credit Act (NCA). This means that all credit providers have to do a rigorous check on whether you can afford the repayments before providing cash.

However, there is no single solution that suits everyone and works out best will depend on how quickly you need the cash, how much you need, and whether you can actually stick to repayment schedule.

Understanding Your Borrowing Options Under the National Credit Act (NCA)

In South Africa, the National Credit Act is designed to protect consumers from predatory lending tactics and ensure responsible borrowing. All credit provider in South Africa needs to be registered with the NCR to give any type of loan.

Lenders also need to verify the stability of your income during the application process to satisfy the NCA’s affordability criteria. The NCA has also strictly capped the maximum interest rates and administrative fees that lenders can legally charge in a credit agreement.

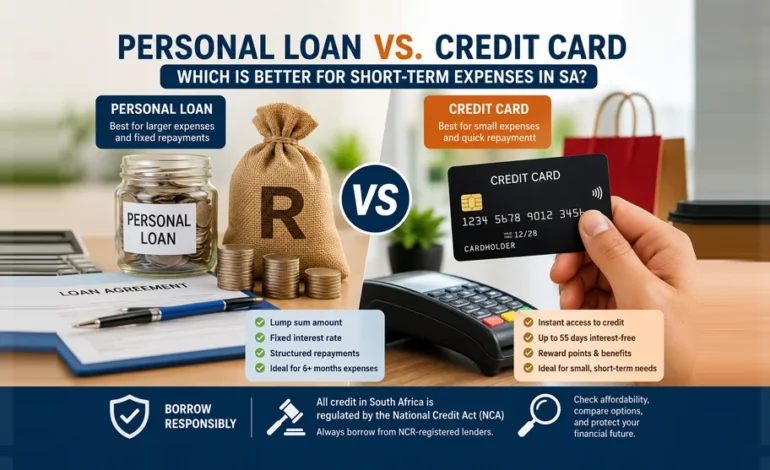

When to Choose a Credit Card for Short-Term Needs?

A credit card is a revolving credit facility, which is best suited for small expenses you can clear rapidly, and most South African banks offer up to 55 days’ interest-free period. And if you can pay the full statement balance before the due date, the cost of borrowing will be effectively. The main benefits of credit cards include:

- It provides instant access to pre-approved funds without a new application.

- You get an interest-free period on card swipes, usually up to 55 days.

- It also gives you earning potential in the form of FNB eBucks, Standard Bank uCount or Nedbank Greenbacks rewards.

However, cash withdrawals from a credit card can charge you a heavy interest rate from the moment you get money from the ATM, as there is no interest-free period for the cash-advance.

When a Short-Term Personal Loan Makes More Financial Sense?

An online personal loan hands you a lump sum that you have to repay over a set period of time, which usually ranges from 6 to 72 months. This is often a better option for larger capital requirements that cannot be settled in a single monthly paycheck, and these loans also offer lower, fixed interest rates compared to the penalty rates of revolving credit. By choosing a short-term personal loan, you get many benefits, including:

- The payments are structured and predictable, so you can plan your budget more precisely.

- You will find a lower interest rate because of long-term borrowing.

- The fixed end date also does a great job in building financial discipline.

However, you should keep in mind that the upfront cost is huge, because lenders can legally charge you an upfront initiation fee of up to R1,050 plus 15% VAT and a monthly service fee, which is capped at R69 inclusive of VAT.

Key Factors to Consider Before Applying for Credit

It is important to compare the core structure of both financial products before committing to debt.

| Feature | Credit Card | Personal Loan |

| Best Use Case | Fast, small expenses cleared in 30-55 days. | Larger, planned expenses over 6+ months. |

| Maximum Interest Rate | Up to 29.25% (Repo rate linked). | Typically 15% – 29.25% (fixed or linked). |

| Initiation Fees | None on standard purchases. | Up to R1,050 + VAT. |

| Monthly Fees | Flat monthly account fee (R40-R100). | Up to R69 (VAT incl.) service fee. |

| Repayment Term | Flexible, revolving. | Fixed (e.g., 6, 12, 24 months). |

The Impact of Your Choice on Your Credit Score – Personal Loan vs. Credit Card Advance

Credit bureaus like TransUnion and Experian track how you manage both revolving and installment credit. High credit card utilization using more than 30% of your available limit negatively impacts your credit score.

A personal loan adds installment credit to your profile. As you make consistent, on-time monthly payments, this builds a strong track record of debt management. Alternatively, taking a cash advance on a credit card can sometimes signal financial distress to banking algorithms if not cleared quickly.

How to Verify Your Lender with the NCR?

Never, borrow money from an unregistered entity, commonly known as a “loan shark” Illegal lenders operate outside the NCA, charging extortionate interest and using unlawful collection tactics.

Always ask for the lender’s NCR registration number (NCRCP1234), you can verify this number instantly be searching the official National Credit Regulator website database. Legitimate lenders will always mandate an affordability assessment and provide a pre-agreement quote outlining all costs in ZAR.

Which is better personal loan or credit card?

Before applying for any of them, you should verify how they compare their pros and cons against each other, to get the most from your budget.

Pros and cons of Credit Card:

| Pros | Cons |

| Convenient way of repayment | Risk of overspending |

| Potential debt | Really high interest on late payments |

| Travel perks and reward points | Can also damage your credit score if used irresponsibly. |

| Can build credit score, if used responsibly |

Pros and Cons of Personal Loan:

| Pros | Cons |

| No collateral requirement | It lacks repayment flexibility |

| Quick access to Funds | High additional Fees |

| Fixed monthly installments | It can increase the debt burden |

| It disburses a single large amount at once | You cannot reuse credit without repaying the first loan. |

To sum it up, for smaller purchases you can comfortably pay off in two months, credit cards are an option, but for anything that can take more than a year to settle, getting a fixed-rate personal loan is the better option. It allows you to maintain a monthly cash flow and tackle the unexpected expenses stress-free.

FAQs – Personal Loan vs. Credit Card Loan:

Is it cheaper to use a credit card or a personal loan for a small emergency?

If you are in a position to repay the amount within the 55-day interest-free window of a credit card, then using one is essentially free of interest. While using a personal loan, you may have to pay an initiation fee and monthly service charges right from the start, which makes a personal loan more expensive for small and short-term emergencies.

Does taking out a personal loan affect my credit score differently than a credit card?

Yes, they affect your credit score differently, as a personal loan is an installment account that rewards you with a good credit score when you make timely monthly payments. While maxing out a credit card significantly increases your credit utilization ratio, that can temporarily lower your credit score until the balance is reduced.

What is the “budget facility” on a South African credit card?

The “budget facility” on South African credit cards allows you to transfer larger purchases into a separate installment plan directly on your credit card. You can then pay off this amount over a chosen period ranging from 6 to 60 months instead of being stuck to a standard 30-day billing cycle.

How do I know if a lender is legitimate in South Africa?

If a lender is registered with NCR, they are required to display their registration number on their website or in a physical branch, and you can use the NCR’s online website to verify their legitimacy.

What is an affordability assessment?

Affordability assessment is a calculation mandated by the NCA that all legitimate lenders must perform. This means they review your net income, living expenses, and all your existing debts to determine whether you can afford the loan repayments without severe financial hardship.

George Desipris is an expert and passionate freelance content writer with 10+ years of experience in creating informative content for various websites, blogs, and other platforms. George is specialized in niche related to finance, especially in investment and trade.

Their writing hook the readers and never let them to search more about the topic. His articles also featured on various news websites like New York Times and Bloomberg. In addition, George Desipris enjoy chess and badminton like sports. He is always try to broaden their knowledge and vision by using his creativity skills.